When should you begin to withdraw your Social Security benefits? It will depend largely on your current and future financial situation.

The earliest you can begin drawing your benefits is at age 62, but it is important to know that you will only be getting 75% of your total benefits if you begin drawing that early.

Early benefits can pay off

There are instances where taking early benefits pays off despite the reduced monthly check. No one can predict how long you’ll live, but if you’re facing a potentially significant reduction in life expectancy and are short of income, taking Social Security early may be appropriate.

Why take it early? A Bridge to Medicare

Remember that while you are eligible for reduced Social Security benefits at 62, you won’t be eligible for Medicare until age 65, so you will probably have to pay for private health insurance in the meantime. That can eat up a large chunk of your Social Security payments.

If you are retiring before age 65, then you may consider turning on Social Security to help pay for health insurance costs. Today, health insurance (not subsidized by the state of Florida or the county) can run $670 per month for an individual and up to $1,700 per month for a family. Please check with your Human Resources Department to find out what the average individual and family are paying for health insurance before age 65.

Once you reach the age of 65, then you become eligible for Medicare, federal health insurance coverage at age 65.

What’s your break-even?

If you want to start Social Security before your full retirement age, you should calculate your break-even age to better determine when you should start drawing Social Security.

Your break-even age occurs when the total value of higher benefits (from postponing retirement) starts to exceed the total value of lower benefits (from choosing early retirement).

Here’s an example: If you are eligible to collect a reduced $900 benefit at age 62 plus 1 month, and your benefit would increase to $1,251 at age 65 and 10 months, your estimated break-even age is 75 years and 5 months.

If you expect to live beyond that age, it would be financially worth your while to delay drawing benefits. Check out the Social Security Administration’s life expectancy calculator to help you decide.

When it comes to calculating a start date for Social Security benefits, however, there’s not an age that’s appropriate for everyone. Consider your own financial need, health. and post-retirement plans before making the call.

The downside of claiming early: Reduced benefits

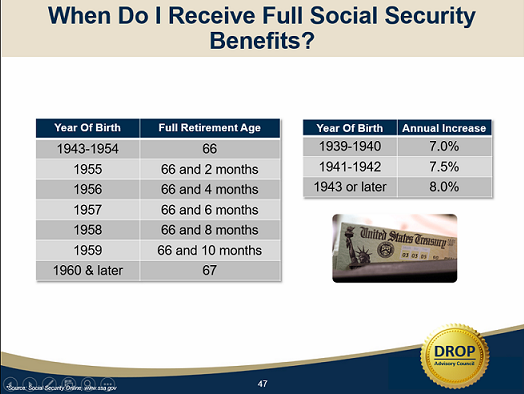

Generally, it’s best to postpone Social Security benefits at least until you reach full retirement age, which is determined by the Social Security Administration.

If you are able to hold off on drawing your benefits until you reach full retirement age, then you will receive 100 percent of your total benefits. Also, each year you hold off on drawing your benefits, the lifetime benefit increases 8 percent every year until you reach age 70.

Collecting Social Security early will cost you

If your full retirement age is 67, your Social Security benefit is reduced by:

- About 30 percent if you start collecting at 62.

- About 25 percent if you start collecting at 63.

- About 20 percent if you start collecting at 64.

- About 13.3 percent if you start collecting at 65.

- About 6.7 percent if you start collecting at 66.

Source: Social Security Administration

Social Security is like longevity insurance. It’s a stream of payments that will not stop throughout your life, so delaying your benefits to keep those payments as large as possible forms a helpful base to your retirement plan.

For example, if your full retirement age is 66, but you delay getting Social Security until 67, you’ll receive 108 percent of your monthly benefit. If you wait until age 70, it jumps to 132 percent.

If you plan to work during retirement, you have another incentive to delay collecting Social Security. Earning too much at a job after you begin collecting Social Security can negatively affect your benefit.

If you are under full retirement age for the entire year, the government deducts $1 from your benefit payment for every $2 you earn above the annual earnings limit. For 2019, the earnings limit is $17,640.

In the year you reach full retirement age, your benefit is reduced by $1 for every $3 you earn above $46,920 (in 2019) until the month you reach full retirement age.

You will also owe Social Security and Medicare tax on your earnings, even if you are already receiving benefits.

Benefits of working longer

Many people want to retire as soon as it is financially feasible to do so, but if you leave before your DROP period ends, consider the DROP and pension money you may give up if you stop working full-time and take Social Security at 62.

Tip: Women often live longer than men, and are more likely to depend on one income when they are older. Don’t make the mistake of coupling your decision to leave the workforce with your Social Security claiming strategy. Remember, by the time you get into your 80s, you have fewer financial options, so don’t jump at the first opportunity to claim Social Security at age 62 just because you may want to quit your current job.

If you have any questions, please contact the DROP Advisory Council. Please fill in the form below: